When trying to pick a stock to achieve alpha and find absolute returns, regardless of market movements, you would look for indicator misgivings that do not truly reflect the intrinsic value of a stock. You would need to search for an opportunity where the street-wide view is wrong, and accordingly sustain a variant view, and search for a stock that is undervalued.

This could be achieved by identifying inefficiencies, (such as information gap or low liquidity) mispricings, asymmetric risk/reward, and companies with high dispersion resulting in significant performance differences. It could be a catalyst driver, such as earnings reports, analyst ratings revisions, product launches, regulatory approvals or changes, M&A or spin-off companies, or industry data reflection.

WesBanco may be a prime option for this. Evidence presented here will support the conviction that WesBanco is quietly trading at a discount, while other brand names are taking up the market’s attention.

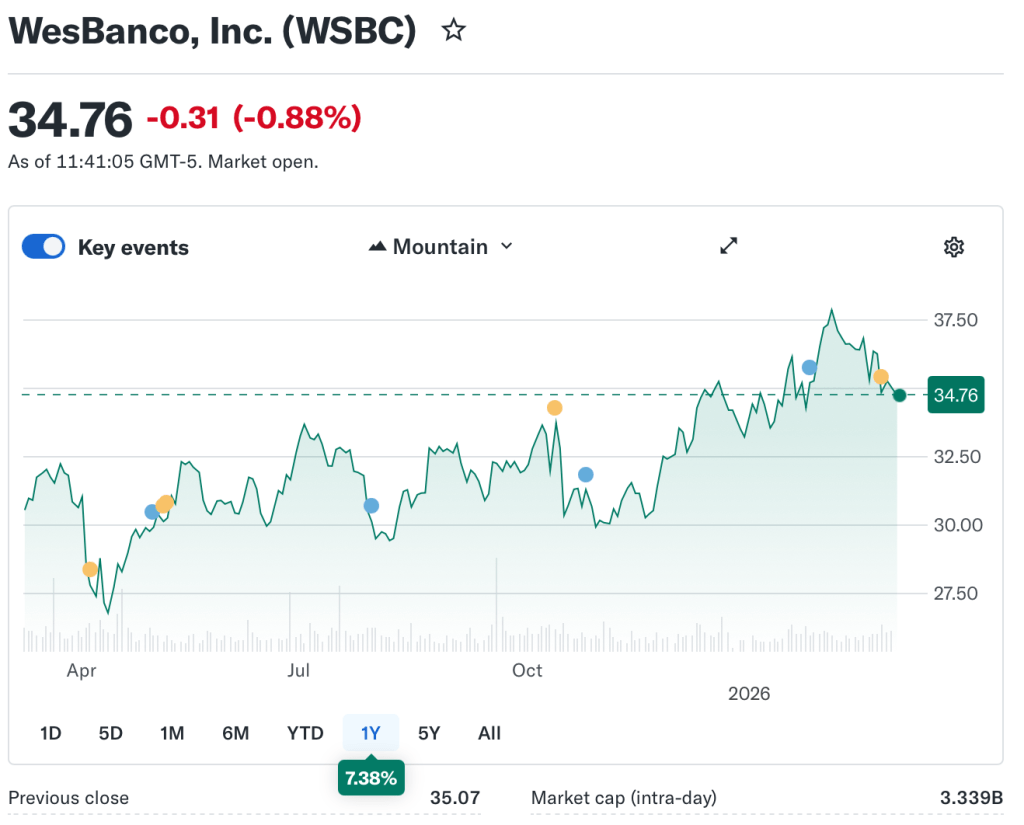

WesBanco is a mid-cap American regional banking holding company, founded in 1870 based in West Virginia. Through a sturdy number of acquisitions, it has built a strong presence in nine states: Kentucky, Maryland, Michigan, Ohio, Pennsylvania, Tennessee, Virginia, and West Virginia. Their business model focuses on community and retail banking, commercial banking, plus wealth and trust services. The company services 400,000 customers, and 50,000 business relationships. The market cap is 3.41 billion USD, with a share price of 34.76 USD, which over the past year has only increase 1.34%. The 1-year estimate is $40.50.

Yahoo Finance ranked Wesbanco as one of the top US equities trading at the highest discount rate, currently at 47.7%, with an estimated fair value of $68.84. The fair value figure displays an estimated ‘true intrinsic’ value of stock based on fundamental analysis, earnings, growth and assets.

Assessing first the stock data, the EPS share is a favourable position with the full year adjusted $3.40, a 45% YonY from the previous year (or $2.33 diluted EPS). EPS for Q4 2025 was $0.84, which is up 18% YonY. EPS is net income divided by shares outstanding; it tells of how profitable the company is per share. EPS is not just a static figure to be taken objectively; EPS quality should be considered. EPS YonY growth, 3-5 EPS CAGR, and forward EPS estimates can also be looked at, to give a broad subjective view. An EPS could be flat for 5 years, but to achieve alpha these figures could be considered to conclude a subjective view on an equity. Wesbanco has strong EPS YoY growth as evidenced.

Considering other markets’ measurable data, Wesbanco’s 5-year monthly beta is 0.78. This beta measure being below 1, means Wesbanco stock has been less volatile over the past 60 months of trading, compared to the market average. Accordingly, with the aim of generating risk-adjusted returns, based on the beta, Wesbanco offers lower systemic risk stocks, during a bearish market in times of market volatility than other stocks. However, from the lens of an asset manager, Wesbanco may not be seen as a strong macro beta play. Although the downside of this equity and low beta position is a regional bank may be highly sensitive to interest rates and credit spreads.

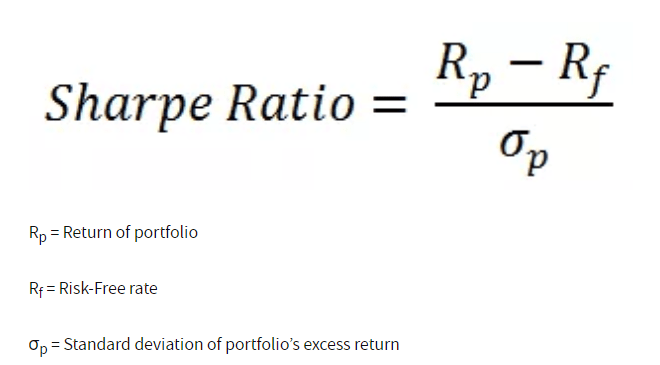

Wesbanco records a 1-year Sharpe ratio of -0.53-, and a 5-year Sharpe ratio of +0.31. The former negative ratio translates into on paper that investing in this stock in the short term, means you are taking on a high volatile risk for a return lower than what you would get for a guaranteed, risk free or very low risk investment. The 5-year latter ratio being positive displays a slightly different picture over the long term, the stock risk adjusted returns are somewhat mildly better. If the 5-year beta were above 1.0 or 2.0, this would be considered very good. For example, if WesBanco returns 12% over the next five years with a beta of +0.31, but another stilled returned 12% but with a beta of +0.05, Wesbanco would be deemed superior, from an asset manager’s perspective.

However, when only downside risk is analysed with the sortino ratio, the 1-year sortino ratio is at -0.84 is much lower. Sharpe ratio considers the total volatility to the market, Sortino considers only downside volatility. The sortino ratio should not be taken as objectively bad. The important caveat is comparing this to see if this was sector-wide or company specific. Looking at other US regional banks such as, M&T Bank, has a 1-year sortino of -1.12, KRE with -0.56, a BB bank, Bank of America with -1.52. Potentially this downside volatility is normalising and may be due to banks often being sensitive to depositor confidence. Additionally, a 1-year negative sortino can often reflect stress or sector rotation and be less representative of structural underperformance.

The high forward dividend and yield of 4.31%, with an estimated payout of $1.52 per share. The forward dividend is high which compared to S&P 500 usually sits around 1-2%, but a 4-6% yield is common for stable regional banks. The PE ratio (TTM) of 15.53 for a stock is considered good, higher than average for the banking sector. Investopedia reports that the P/E of major US national banks, is on average 8.46, with smaller regional banks on average being 13.50. The P/E ratio can tell a narrative of how much investors are willing to pay for every dollar of profit a company will deliver. This slightly higher figure for WesBanco infers that investors expect high growth rates.

In terms of earnings growth potential for the company, the completion of the acquisition of Premier Financial Corp, worth $959m in an all-stock deal in early last year, the company expects synergies and EPS accretion to deliver. Wesbanco projects $1.7 billion revenue, in tandem with its earnings to boost its earnings from $125.2 million to $821.3 million. This equates to a 35.2% revenue growth. This is possible since, the bank’s annualised revenue growth has upped 27.4% over the last two years, which is as such higher than its five-year trend. Yahoo Finance affirms demand has accelerated for the bank.

However, intrinsic risk that may stop the bank achieving its projects is its high commercial real estate exposure. As of December 2025, the banks total assets grew to $27.7 billion, with total portfolio loans equalling $19.2 million, with Commercial Real estate payoffs, coming to $905 million for the year 2025. Contestably, the bank’s concentrated regional footing, in the Midwest, may make the firm vulnerable to regional economic downturns.

In rebuttal to this, the regional positioning may aid as a growth factor for Wesbanco, when tied to the expectation of two more 25bps rate cuts expected by the Fed for the US for this year. Regional banks can benefit from steady monetary policy loosening, when the interest earnt on loans, and the net interest margin (essentially the interest they pay on deposits) holds up. If the loosening is steady, this means Wesbanco will be able to maintain healthy margins, whilst credit demand picks up. This rate cut aligns with continued economic growth tin he US expected for 2026, supporting especially consumer confidence and business spending, helping service a bank with this focus.

To conclude, WesBanco presents a compelling and nuanced case for a potentially undervalued regional banking equity. With strong financial growth projections, and expectations the stock with rise in value evidenced by full year adjusted EPS of $3.40, a 45% YonY from the previous year, forward dividend and yield of 4.31% with a payout of $1.52 a share. The potential mitigants to take into consideration in your own assessment include the negative 1-year Sharpe ratio and negative 1-year Sortino ratio, while too the commercial real estate exposure. However, this may be nulled by the immersion of its acquisition with Premier Financial Corp, which could help it achieve its ambitious earnings goal of $821.3 million.

Disclaimer: Not financial advice

Sources:

https://www.investopedia.com/terms/d/dividendyield.asp

https://finance.yahoo.com/news/february-2026s-value-picks-stocks-113805029.html

https://uk.finance.yahoo.com/quote/WSBC/

https://www.tipranks.com/news/catalyst/why-wesbanco-shares-are-sliding-despite-buy-ratings

https://finance.yahoo.com/news/still-value-wesbanco-recent-share-150724648.html

https://finance.yahoo.com/news/makes-wesbanco-wsbc-investment-choice-142142349.html